The Changing Nat Gas Market

June 24, 2025

North America’s liquefied natural gas (LNG) export capacity is on track to more than double between 2024 and 2028 to 24.4 Bcf/d, if projects currently under construction begin operations as planned. Between 2024 and 2028, EIA estimates LNG export capacity will grow by 9.7 Bcf/d in the U.S. Where will the feed stock come from? According to multiple sources, the majority of new gas pipeline capacity under development in the U.S. will feed LNG exports rather than serve domestic demand. The Center for Energy & Environmental Analysis reports that the total volume of U.S. natural gas exports, both LNG and pipeline, will exceed the total amount of natural gas consumed by the U.S. industrial sector in 2025.

The Henry Hub spot price in the latest EIA Short Term Energy Outlook forecast averages about $4.00 /mmbtu in 2025 and $4.90/mmbtu in 2026, compared with $2.20/mmbtu in 2024. EIA said that higher natural gas prices in 2025 and 2026 are the result of strong export growth that persistently outpaces U.S. natural gas production.

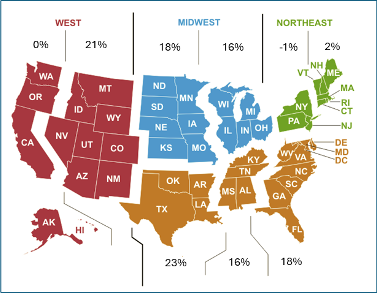

EIA forecasts the U.S. industrial average for natural gas prices to increase year-over-year in 2026 by double digits in ERCOT and parts of PJM. Lower prices prevail in the Mid Atlantic. New England faces a modest increase.